The Chaotic State of Payment Methods in Japan

Published on

There are so many ways to make payments in Japan.

The following screenshots show the list of supported payment methods at some convenience stores in Japan.

7-Eleven:

Source: ご利用可能なお支払方法|セブン‐イレブン~近くて便利~

FamilyMart:

Source: ご利用可能な決済サービス|サービス|FamilyMart

Despite there being so many supported digital payment methods, none of them are dominant and 57.7% of payments at 7-Eleven are cash (as of November 2020).

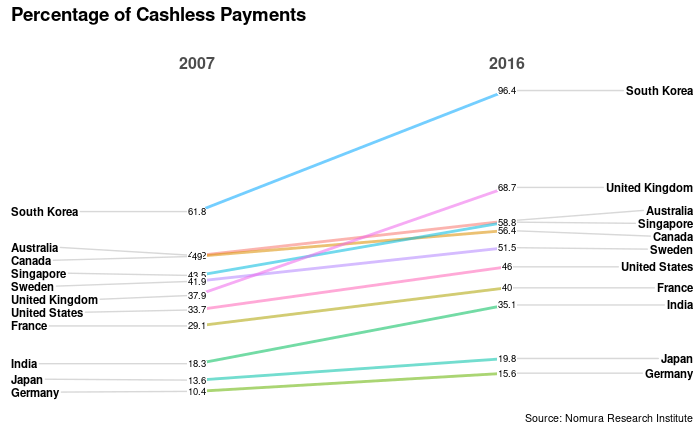

Cashless payments are increasing in Japan like other countries, but the percentage is still relatively low (It reached 26.8% in 2019):

Source: Nomura Research Center

Why is this the case?

Electronic Money Usage in Japan

According to the Zoo Money article なぜ日本の電子マネーは先進的なのに「キャッシュレス化」が進まないのか? (Why Japan is advanced in electronic money but isn’t becoming cashless), electronic money is actually commonly used in Japan, even though Japanese society is far from being cashless.

Electronic money (e-money) is broadly defined as an electronic store of monetary value on a technical device that may be widely used for making payments to entities other than the e-money issuer. The device acts as a prepaid bearer instrument which does not necessarily involve bank accounts in transactions. (European Central Bank)

The article lists 3 main categories of e-money:

- Transportation: Suica, Icoca, Pasmo

- Distribution: Waon, Nanaco

- Independent: Rakuten Edy

Transportation

Many people use IC Cards like Suica and Icoca on public transportation. These cards are mostly issued by train companies in each region.

They are common because they have some clear advantages over using paper tickets:

- You don’t have to go to the ticket machine and buy a ticket each time you go on the train

- You can get on and off wherever you want

- It’s easy to transfer between different lines operated by different companies

- Recharging isn’t any more difficult than buying a ticket with cash

- They are easy to use even for elderly people who aren’t using smartphone apps

These are primarily used for transportation, but can be used to pay at stores and vending machines as well:

Distribution

These are e-money issued by retailers.

WAON

Waon (ワオン) is a Japanese electronic money system introduced by ÆON in April 2007. It is a rechargeable contactless smart card. Like many other smart card systems in Japan, it uses RFID technology developed by Sony known as FeliCa. Its name comes from waon (和音), meaning chord. The card’s official mascot is a white dog. The card reader makes a “waon” sound upon successful transaction, a Japanese onomatopoeia for dog barks. (Wikipedia)

ÆON is a large retail group, so this card is supported at their own stores, as well as many other businesses.

Nanaco

Nanaco (trademarked as nanaco) is a prepaid cash-rechargeable contactless electronic money card used at Seven & I Holdings-owned stores in Japan, which are 7-Eleven convenience stores, Denny’s restaurants, and Ito-Yokado merchandise stores. In addition, Nanaco can be used at more than 7,000 stores outside the company’s group, especially those that are JCM affiliated shops. (Wikipedia)

Nanaco can be used at 739,000 stores as of December 2020.

Independent

Rakuten Edy

Edy, provided by Rakuten, Inc. in Japan is a prepaid rechargeable contactless smart card. While the name derives from euro, dollar, and yen, it works with yen only. (Wikipedia)

Rakuten Edy is supported at over 450,000 stores: List of stores

E-money is very common

There were 66.7 million Suica cards, 64.5 million Waon Cards, and 53.5 million Nanaco cards issued as of 2017, so having some of these cards is very common considering Japan’s 120 million population.

In addition, reward points are common, so there are popular digital reward programs that can be used for payments. Some examples are d-POINT and T-Point.

E-money is well supported by digital wallets, such as Apple Pay and Google Pay. Both platforms seem to be designed for use with a Credit or Debit Card at least in the United States.

However, the Japanese pages promote the use of transportation IC cards like Suica and Pasmo near the top of the page:

https://www.apple.com/jp/apple-pay/

https://pay.google.com/intl/ja_jp/about/

Using e-money cards for transportation and paying for products was a common use case, so it is supported on these platforms to allow users to just use them with your phone.

However, despite e-money being common, many people still use cash every day.

Because there are so many e-money services, it’s costly for businesses to support everything. As a result, there aren’t any digital payment methods that are supported everywhere, and people just end up using cash because they don’t have to worry about whether it’s supported or not.

To make Japanese society more cashless, it may be necessary for banks and other businesses providing e-money to work together to create a system that is easy and inexpensive for businesses.

Credit Card Support

In many countries, credit cards are the dominant digital payment method that most businesses support. Why is this not the case in Japan?

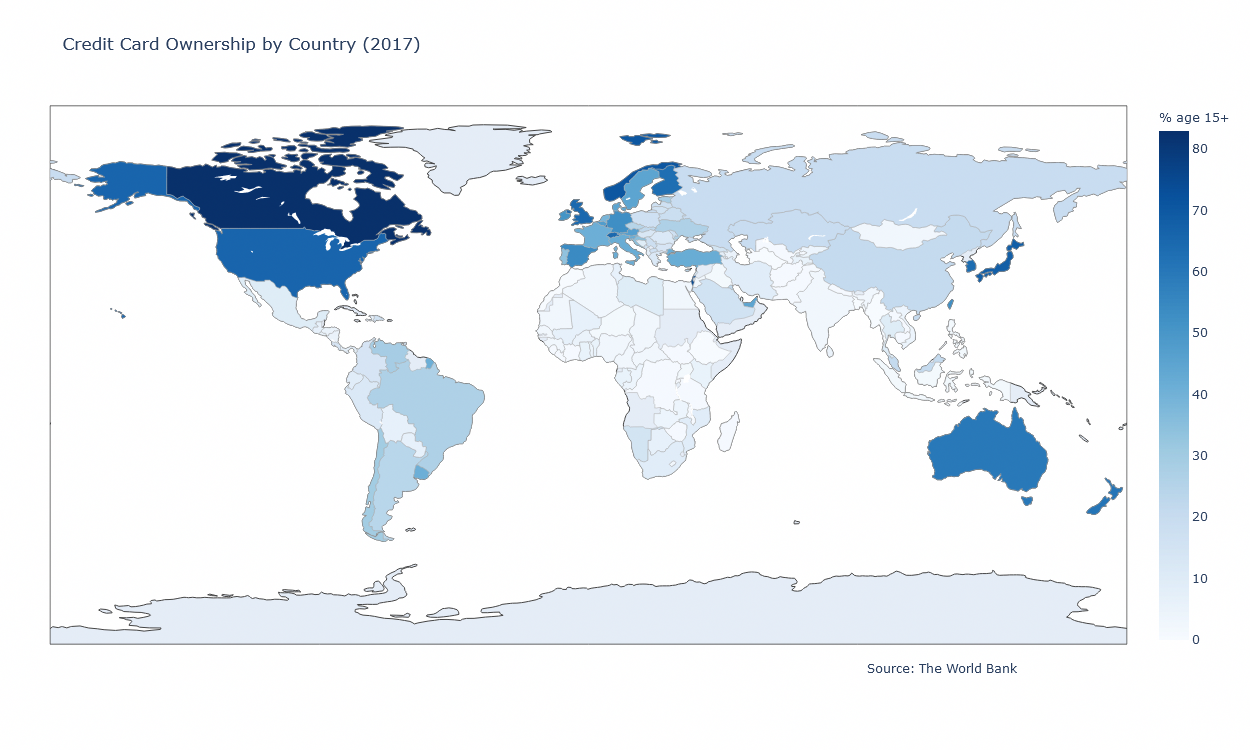

In Japan, many people actually have credit cards.

Japanese actually have as many credit cards as Americans do. Research shows that there are 258 million credit cards currently issued in Japan. This means that every Japanese adult has approximately 2.5 credit cards, which is very close to how many Americans have per person (2.6 credit cards).

Source: The World Bank

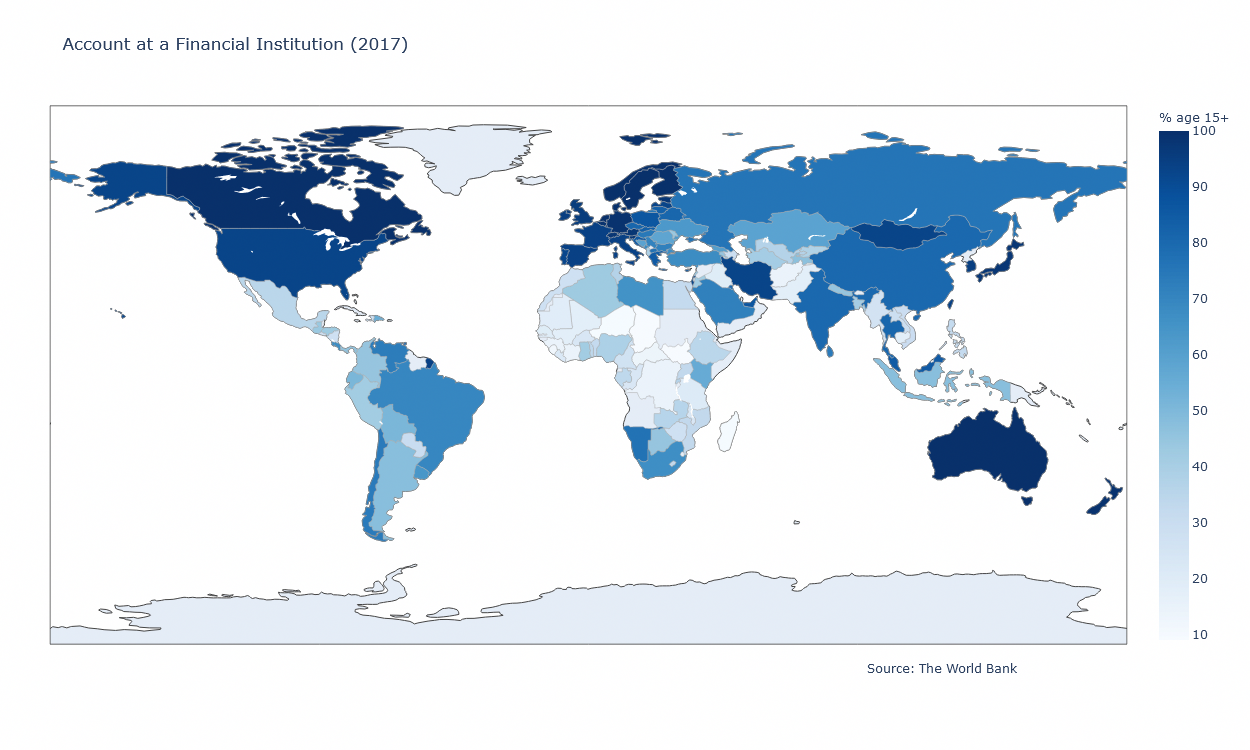

Most people also have accounts at financial institutions unlike many other countries.

Source: The World Bank

However, in Japan, it’s not that people don’t have access to credit cards or other electronic payment methods—they just don’t use them as much as when paying at physical stores.

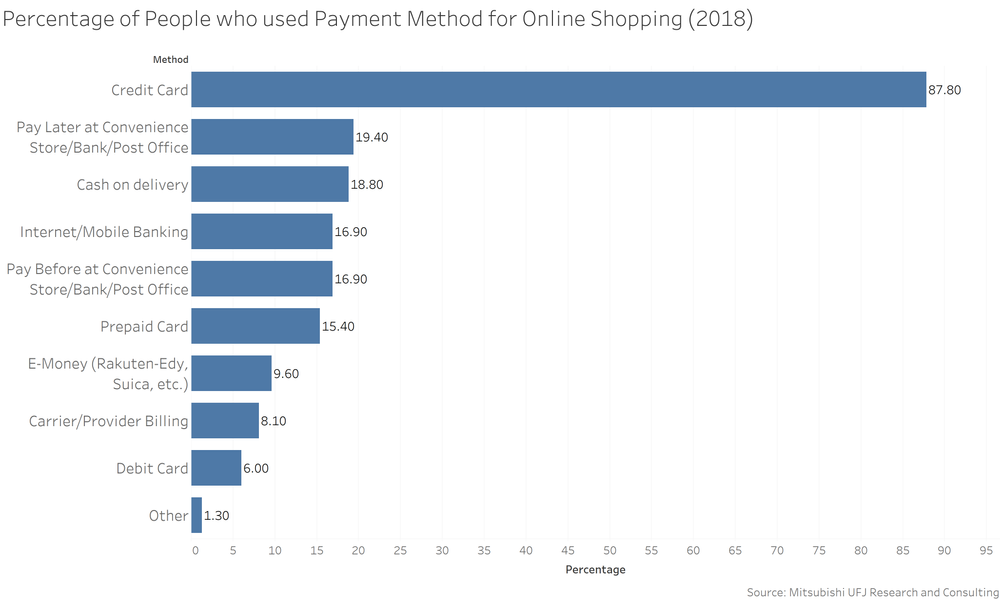

This is just one survey by MUFG, but most people seem to use credit cards for online shopping, and people certainly shop online in Japan.

Source: MUFG

Credit cards are just not well supported at physical locations for business reasons and many people prefer to pay with cash when they’re paying in person.

Business Perspective

The major issue from the business perspective is that credit card fees are expensive for small businesses:

Processing charges normally hover around 2-5% in Japan, reportedly higher than most countries.

”Smaller retailers have profit margins of around 2 percent on average” so small businesses can’t afford to support credit cards.

Some industries have good support, but many others like the medical industry have poor credit card support. Over 80% of hotels and golf clubs support credit cards, but only 49% of hospitals support credit cards, and only 16.5% of local clinics support credit cards. A large percentage of patients are old, so credit card usage is low, and they may not feel that it’s necessary to support credit cards.

With the aging population, it will become even more important to make everything more efficient, and cashless payments may be a good way to do that, but the support is still not yet great due to business reasons.

Consumer Perspective

There are also reasons for why many consumers prefer cash. According to a survey by NIRA, the top 5 reasons for preferring cash in physical stores are as follows:

- Worried about over-spending because any method other than cash doesn’t feel like actually using money

- Worried about security

- Not necessary

- Worried about loss and theft

- Difficult to manage account balance and passwords

Some of these reasons probably aren’t unique to Japan, but many people in Japan don’t always use cashless methods because it’s “not necessary” (#3). When there isn’t a cashless payment method that everyone uses, figuring out what service to use, setting it up, and checking whether it’s supported each time you want to pay might be more annoying than just using cash.

Of course, it can still be annoying to deal with cash, and it might be more efficient to use cashless payment methods, but it’s at least a “decent” payment method for most people:

Moving away from cash doesn’t necessarily speed up commerce, since Japanese retailers are crazy good at counting change.

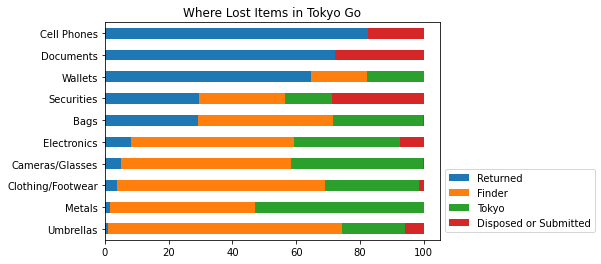

People also feel safer carrying larger sums of money, and there’s a reasonable chance you’ll find your wallet even if you lose it, with majority of lost wallets in Tokyo being returned to the owner1:

Source: Tokyo Metropolitan Police Department

Debit Cards

Debit cards are not commonly used in Japan. In this 2020 survey by JCB, only 8.8% of people replied that they used a debit card.

According to the Bank of Japan, many ATM cards have a debit functionality (J-Debit) so Japanese people have more debit cards than many other countries2. However, they aren’t used much as debit cards because it’s relatively easy to get a credit card in Japan, and cash and e-money have been more commonly used for small transactions.

One theory by Junko Itonaga and Hideyuki Tanaka of the University of Tokyo is that personal checks are not commonly used in Japan, so people don’t have a habit of directly making payments from their bank accounts (with the exception of bank transfers), and as a result debit cards weren’t a good fit in the lives of Japanese people.

Effect of Government Campaigns and COVID-19

The usage of cashless payment methods increased after a government campaign during 2019 and 2020:

Also contributing to the growth was the program to give reward points to people using cashless payment methods, introduced by the government in October last year to mitigate the impact of the consumption tax increase from 8 percent to 10 percent in the month.

With COVID-19, there has been an additional increase in the number of users of cashless payment methods and online shopping.

QR Code Payment Apps

QR Code Payment apps are new, but are growing, and they are competing to win over more users. The users scan a QR Code to complete the payment.

They are seen as an alternative to credit cards:

Introduction of QR code payment, on the other hand, does not place a significant burden on vendors in means of initial investment, as has been evident in the technology’s rapid spread in China. Attitudes are also changing, as the young “digital native” generation in particular has begun to view mobile payment as convenient and safe.

PayPay

PayPay utilizes the payment technology of Paytm from India:

PayPay Corporation, a joint venture established by SoftBank Corp. (“SoftBank”) and Yahoo Japan Corporation (“Yahoo Japan”), today announced that the company will launch “PayPay” smartphone payment services using barcodes (QR code) in fall 2018. PayPay Corporation will team up with India’s largest digital payment company Paytm, a SoftBank Vision Fund portfolio company, to utilize Paytm’s technology and expertise in mobile payments.

They held a 10 billion yen giveaway campaign, where they first gained many users.

PayPay Corporation, a joint venture of SoftBank Corp. and Yahoo Japan Corporation is scheduling a “10 Billion Yen Giveaway Campaign(Open in a new window)” during December 4, 2018 to March 31, 2019 which a partial or full cashback is given to payment transactions made by their mobile payment service PayPay

They have over 35 million users as of Janurary 2021.

Merpay

Merpay, a smartphone app service, makes paying for merchandise on an EC site easy and seamless.An online payment can be made by using the sales balance* on Mercari, reward points, Merpay balance, charge-type payment and, Merpay Smart payment (aggregate payment to the next month, eligibility standards apply). (GMO)

LINE Pay

https://pay.line.me/portal/jp/main

Line introduced Line Pay worldwide on December 16, 2014. The service allows users to request and send money from users in their contact list and make mobile payments in store. The service has since expanded to allow other features such as offline wire transfers when making purchases and ATM transactions like depositing and withdrawing money. Unlike other Line services, Line Pay is offered worldwide through the Line app. (Wikipedia)

Rakuten Pay

It is a payment method that allows Rakuten members to pay for goods and services with their Rakuten ID…Users of the Rakuten Pay (Online Payment) can easily and safely make payments by just entering their Rakuten ID and password. Also, they can earn and use Rakuten Super Points when making online purchases. (GMO)

Chinese Payment Apps

Many stores in Japan support the two major digital payment platforms in China—Alipay and WeChat Pay.

Over 90% of people in China’s largest cities use WeChat Pay and Alipay as their primary payment method, with cash second, and card-based debit/credit a distant third.

The Japanese Alipay website is targeted towards business owners who want to support payments by Chinese tourists—not individual users in Japan.

"The Payment App Most Used by Chinese Consumers Alipay—Easy to Install"

You can sometimes see Alipay and WeChat Pay logos in Japanese stores.

Cryptocurrencies

There are stores like Bic Camera that support bitcoin, but it’s still not a very common way to pay for products.

Some think that Japan could see widespread usage of cryptocurrencies before another digital payment method becomes dominant:

With the government’s pressure to go cashless, and little competition from credit cards and other forms of e-payment, Japan could leapfrog the technology underlying today’s electronic payment networks and go straight to blockchains.

If this happens, it might be somewhat similar to how Alipay and Wechat Pay became dominant in China skipping credit cards:

In China, the situation is quite different. Many people have never seen — let alone used — a credit card, as mobile platforms like Alipay, offered by Alibaba Group Holding affiliate Ant Financial, and WeChat Pay, operated by Tencent Holdings, gained traction before credit cards had a chance to catch on.

At the moment though, the average person doesn’t feel the need to use cryptocurrencies the way people in Venezuala do:

Many Venezuelans are using Bitcoin to convert their bolivars, which are being permanently devalued by hyperinflation, to keep something of value

The Japanese economy has been stagnant for decades, but the yen is still considered a safe currency, and Japanese people don’t have major problems with the currency.

Things may change in the future, but it doesn’t look like cryptocurrencies will become dominant right away because they don’t provide a clear advantage over the alternatives to the average person in Japan.

Chaos Map of Payment Methods

There are so many ways to categorize the various payment methods. This one is appropriately titled as a “Chaos Map.”

Ultimately, the fact that digital payments are so confusing in Japan might be why many people still prefer cash.

Best Payment Methods

People who live in Japan each have their own choice of payment methods, but the basic combination for many people would be prepaid IC cards for transportation, cash in physical stores, and credit cards for online shopping. Tourists can probably do the same thing.

Regardless of what your main payment methods are, it’s always safe to have cash because many stores still only support cash.

Otherwise, IC Cards like Suica and Icoca can be purchased easily, so they’re convenient to have during your travels.

Software Used

- Python (pandas, matplotlib, plotly)

- R (CGPfunctions)

- Tableau

Footnotes:

1: This is from the Ehime prefectural police website, but the category “Securities” seems to include gift cards, train tickets, IC Cards, etc.

2: The data from the Bank of International Settlements (BIS) Publication indicates that there were 3.3 debit cards issued per person in Japan as of 2016. This is higher than the 0.96 in the United States, 1.5 in the United Kingdom, 1.9 debit in Singapore, and 3.2 in South Korea.